"Wave Goodbye to

Retirement Worries:

An Investment Secret Safer Than Stocks - And Potentially More Lucrative"

Discover The Revolutionary Retirement Model Transforming The Way Americans

Think About Their Golden Years.

Checks Arrive Each Month Thanks To An Investment That's Safer Than The Stock Market.

Finally, Retire With The Peace Of Mind You Deserve.

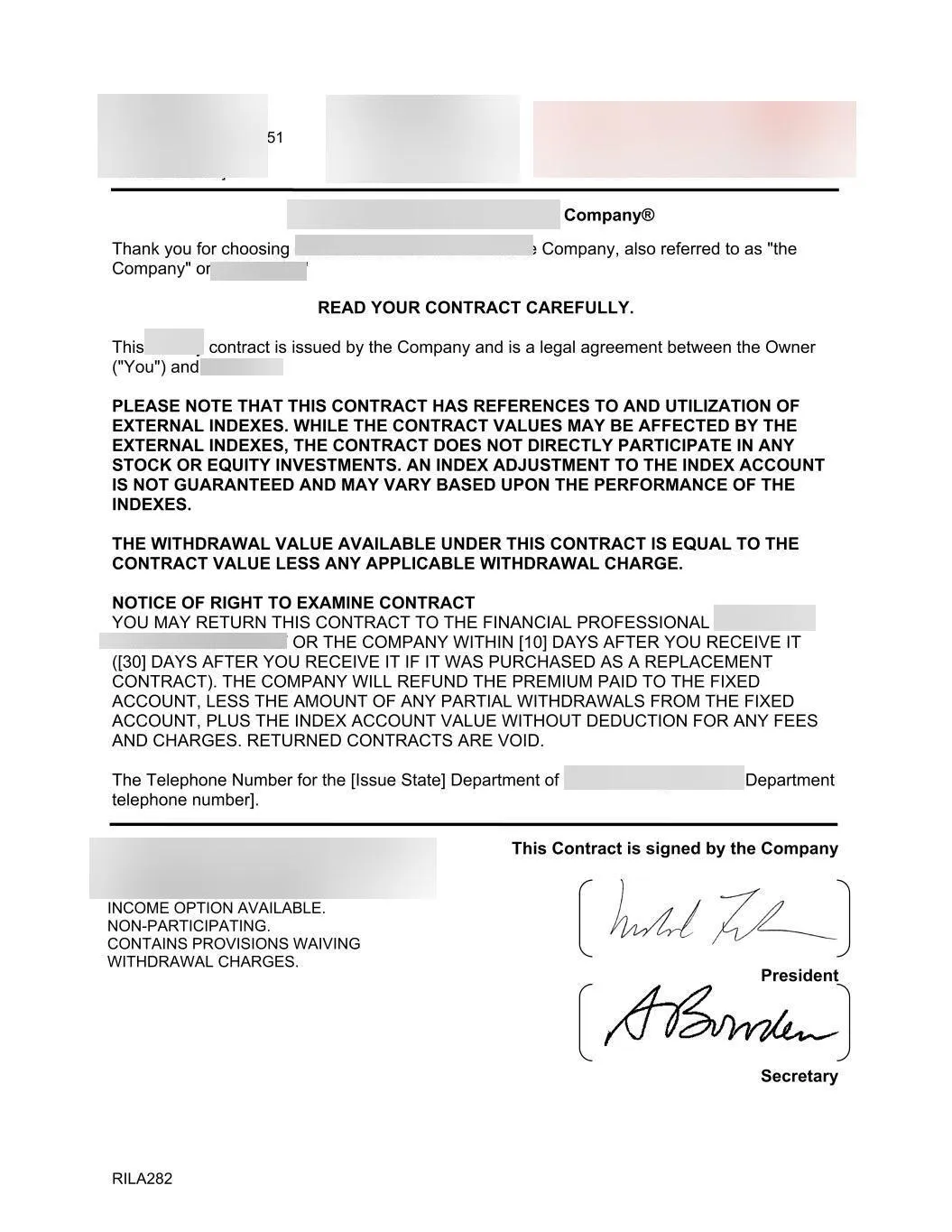

Take a look at this document …

It's a contract, but not a regular one.

Few Americans know you can use this contract to generate reliable income every single month.

In fact, it forces the company issuing it to send you a paycheck every month – no matter what.

And this isn't just for a few months or years...

The Company MUST Pay You

For As Long As You're Alive.

This is what I call a “Guaranteed Income Contract” – GIC for short. And it’s available to all Americans who know how to set up one.

I will show you how in just a minute.

If you’re entering your golden years…

And you’re ready to kick back… relax… and enjoy the fruits of your lifelong labor….

This contract could let you spend your days worry-free.

You might be wondering if this sounds too good to be true.

I get it.

We've always been told that retirement means 2 things:

1) Either risking our savings in the stock market, or….

2)Relying on Social Security while chipping away at our hard-earned nest egg.

But here's the thing – that's NOT the whole story.

Many financial advisors keep GICs as their little secret.

They set up GICs for themselves… but aren’t sharing them with clients.

In fact, a survey all across the nation found that 89% of advisors and financial professionals use (or plan to use) GICs to secure lifetime income.

So why aren’t they telling you?

Well, you set up a GIC once, and the payments start rolling in every month.

So this “set-it-and-forget-it” income stream means some financial advisors can’t keep whacking your entire account 1% to 2% forever.

So What Exactly Is A GIC?

It's a simple yet powerful concept.

You entrust your money to big, reputable companies.

They use your funds for their business, and in return, they're legally obligated to pay you a steady monthly income.

In short, as long as they hold your money, they pay you.

Best part?

If you ever need to, you can get your money back.

So in a world where interest rates are low… the stock market goes up and down like a rollercoaster… and a recession is possible…

… GICs are more essential than ever.

You see, they're more stable than stocks (since you have the option to get back your funds).

What’s more, they offer better returns than bonds and CDs.

Plus, you have control over how much you get each month.

That’s why Fortune calls them “ the best place for retirement cash”...

Why the New York Times says to use GICs “for more certainty in your retirement portfolio”...

And why Barron’s simply calls them “the new way to retire.”

Look: If you've been smart with your money all along, you deserve to have the resources to master your retirement planning.

That's my goal.

To arm you with the information you need to make the best choices for your future. So…

I Will Share With You ALL

The Facts And Stats About GICs.

Then it’s up to you to decide if you want to use them to fund your retirement.

Imagine waking up each morning with a sense of excitement and freedom. Your days are yours to design.

Maybe you start your day with a leisurely breakfast followed by a round of golf… a painting class… and some quality time with your grandchildren.

Whatever you choose to do is up to you. But what’s important is that YOU choose how to live your life.

And that you have absolutely no money worries.

Thinking about your retirement should fill you with excitement.

It’s a phase of life where you should indulge in hobbies… spend time with loved ones… and maybe even explore those places on your bucket list.

All while knowing that…

ALL Your Financial Needs Are Securely Met.

That’s why, in the next few minutes, I'll share everything you need to get GICs:

- I will show you how they offer a more reliable retirement income compared to traditional methods.

- I will reveal the exact steps to set up a GIC for yourself.

- And I will share the 3 reasons why your well-planned retirement might not be as secure as you think – and how GICs can give you peace of mind in your golden years.

So continue reading as I reveal how you can secure a retirement that's not just survived but thoroughly enjoyed.

The Income Secret I Stole

From Wall Street

My name is Sterling Van Gogh.

In the financial industry, I’m known as "the advisor to advisors."

I've coached over 40,000 financial advisors on how to use GIC's.

And my private clients have paid me up to $47,000 in cash for my work.

Over 50,000 advisors see my content and countless thousands of them seek me out for advice.

Why?

Well, because I'm the guy they call when they need to secure their clients' financial futures.

The reason is simple: I know the ins and outs of creating stable, worry-free retirement plans.

And the cornerstone of these plans is GICs.

Let me explain how I discovered them.

As a young college student, amid the chaos of the 2009 market crash, I created a dividend portfolio yielding 5%.

That was my start into the world of finance.

My path led me through the corridors of power at Merrill Lynch, in the same halls with a slice of their colossal $2.9 trillion portfolio.

Then my career took me to another company (I’m not allowed to share its name).

But I can tell you that it’s a financial behemoth that helps rich Americans preserve and grow their money.

As of 2022, they manage over 1.35 TRILLION dollars worth of GIC's.

And that’s where I learned the

insider secrets

of GIC, from the biggest and best GIC manager in the world.

I've Helped Advisors And Investors

Place Over $113 Million In GICs.

The rewards for this work and more were enough to live the dream life.

Convertible sports cars, a luxury condo in the nicest neighborhood in Denver, and luxury vacations several times a year.

But something felt wrong.

I figured out what it was in 2021… when I witnessed a troubling trend.

I saw how the flood of stimulus money and supply chain disruptions would impact the economy.

So – just like I predicted - the rich got richer.

While the average American grappled with soaring inflation and dwindling savings.

That's when I made a pivotal decision.

To me, uncovering hidden income streams is almost instinctual.

But I recognize that for many, this world of financial strategies seems as complex as a foreign language.

These secrets of wealth generation are typically reserved for a privileged few.

But I believe these strategies should be accessible to all Americans.

So I walked away from the glitz of Wall Street to dedicate myself to helping everyday Americans enjoy financial security.

My passion now lies in helping people like you create passive income streams that change lives.

In fact, my mission is to help over 1,000,000 Americans never run out of money.

It’s thrilling to hear stories of people who’ve used my advice to pay off debts… indulge in dream vacations… or even step into early retirement.

So, here's my pledge:

I'm here to share my knowledge, experience, and passion to help you secure a future where you can enjoy your golden years without worry.

Together, we'll navigate the complexities of retirement planning. Starting with…

Why Your Retirement Is Not As Safe As You Thought

People are living longer than ever before. You might have seen the elites call it a longevity CRISIS.

As if living a long and enjoyable life is a sin.

I believe we should celebrate that Americans who worked hard all their life have more time to enjoy the fruits of their labor.

You see…

Our grandparents could barely imagine living past 70. But here we are, looking at life expectancies that stretch well into our late 70s and 80s and beyond.

It's an amazing feat, but it's also loaded with new challenges.

Our retirement savings need to stretch further, much further.

Take the story of Bob and Mary, a typical couple gearing up for retirement. They've been smart, saving a nest egg of $500,000.

Like many, they've been banking on the traditional retirement plan – Social Security, their savings, and a small pension.

It sounds like a solid plan, right?

But here's the catch.

We're living much longer than the folks who made these plans thought we would.

Bob and Mary, expecting to enjoy their retirement peacefully, are facing a harsh truth.

Even with their carefully saved half-a-million, they're facing…

The Very Real Risk Of Outliving Their Savings.

And it's not just them.

This is a story echoing across the nation.

In today's world, we're not just living longer – we're navigating a financial landscape that's changing rapidly.

Low interest rates, which have lingered for years, are not likely to stay that way.

They're going up! Which means

everything

will be more expensive.

Now you have to stretch that same dollar even further.

And there's another wave coming – the "gray wave" of retiring baby boomers.

It's so massive that it might overwhelm Social Security.

Yes, there are so many retirees that it's possible for Social Security to completely run out of money, and those checks could suddenly stop.

That's a real problem for anyone relying solely on Social Security for retirement income.

Then there's the political factor.

The wrong president in office could have a dramatic impact on the economy.

Imagine policies that lead to even higher inflation or increased taxation, eroding the value of your savings and investments.

Not to mention what the wrong guy in the White House could mean for the stock market.

This alone could make the difference between a comfortable retirement and one filled with financial anxiety.

This is where Guaranteed Income Contracts (GICs) come into play.

They offer a solution to these modern challenges.

By locking in a GIC, you're securing a steady income stream that isn't harmed by high interest rates… political changes… or the strain on Social Security.

For folks like Bob and Mary, this could be a game-changer.

Instead of watching their $500,000 nest egg fluctuate with the markets or diminish with low interest, they could ensure a guaranteed monthly income from a GIC.

This income will continue throughout their lives, giving them financial stability no matter what happens in the economy or with Social Security.

This is the kind of security GICs offer.

They're the answer to living longer without the fear of running out of money.

That’s why the demand for GICs is rapidly climbing well into the Trillions.

According to the Washington Post: “Every year, investors are pouring hundreds of billions of dollars into [Guaranteed Income Contracts].”

So, let me guide you through this.

What are Guaranteed Income Contracts?

Guaranteed Income Contracts, or GICs, are financial tools that millions of savvy investors are turning to for their retirement.

They function just like Social Security should, delivering a steady stream of income right into your bank account each month.

The beauty of GICs, however, lies in their flexibility and higher payout potential.

Unlike Social Security, with GICs, you're in control of how much you receive and when.

Think of GICs as a safer, more reliable version of dividend-paying stocks.

You see, while stocks can offer dividends, they also come with the risk of losing your principal investment.

GICs, on the other hand, safeguard your initial investment prior to income.

This protects you from loss while you can still get stock market like gains.

That alone makes them a secure option for your golden years.

Here’s some compelling data:

During the tumultuous 2007-2008 global financial crisis, a pivotal study by the Wharton Financial Institutions Center revealed the resilience of GICs.

They not only outperformed stocks and bonds but were the best option for those nearing retirement.

The reason?

GICs provided a more stable and higher income, significantly reducing the risk of depleting retirement funds.

But this isn't a one-off scenario.

History has repeatedly shown the strength of GICs during economic downturns.

The American College of Financial Services' research highlights their superior performance during several crises.

From the dot-com crash to the oil crisis of the '70s, and even during the Great Depression.

GICs consistently offered better protection… less volatility… and higher withdrawal rates without the risk of exhausting retirement savings.

That’s why some of the biggest names in finance recommend GICs.

Warren Buffett, perhaps the greatest investor in history, is a proponent of GICs for steady retirement income.

In his 2019 letter to shareholders, he wrote:

"In essence, the world is dividing into two blocs—the financial and the nonfinancial. In the nonfinancial world, you can reasonably expect that, whatever the future may hold, you will receive your paycheck. In the financial world, where you own stocks or bonds, the paycheck is up to you. The best way to assure yourself of a positive outcome is to buy a [GIC]."

Suze Orman, a

personal finance expert and best-selling author, also advocates for GICs.

In an interview with Forbes, she said:

"I think they are the only way that you can get a guaranteed income for the rest of your life, no matter what happens to the stock market, no matter what happens to interest rates, no matter what happens to anything."

David Bach, a financial author and authority in the field, also views GICs as the ultimate retirement income solution.

In his book, “The Automatic Millionaire,” he wrote:

“They are like a pension you can buy for yourself. They pay you a monthly income for as long as you live, no matter what happens to the economy, the stock market, or interest rates."

Despite these endorsements, GICs remain shrouded in mystery for many.

This isn't surprising. GICs are complex financial instruments that require guidance to navigate.

That’s why a study showed that those who understand GICs are 3 times more likely to use them for guaranteed lifetime income.

Also, the study showed that only 1 in 4 average folks truly understand them.

If GICs are new to you, I get it.

But with the right information and guidance, GICs can be demystified and harnessed as a powerful tool for a secure, worry-free retirement.

They can bring peace of mind and stability to your golden years. So your retirement is not just comfortable but also financially resilient.

Why Most People Are WRONG About GICs

As you might have guessed, GICs are popularly known as annuities.

I understand why you might be hesitant about annuities. A lot of people share your concerns.

You're probably thinking that annuities come with high fees, and that’s a valid concern.

In the past, this was often true. But that is changing today.

However, let me say that not all annuities are the same.

For instance, some fixed annuities have annual fees as low as 0.20% to 0.50%, significantly lower than the average mutual fund fee of around 1% or more.

And that's

far lower

than some advisor fees at 1%, 1.5% and yes even 2% every single year, whether the stock market is up or down.

This makes them one of the most cost-effective options for a stable income.

Another worry I often hear is about the returns on annuities.

It's a common belief that annuities don’t provide good returns.

It's true that some annuities, especially older ones, might not have offered the most attractive returns.

But annuities today are designed differently.

And annuities actually benefit from raising interest rates - because that means they'll pay you even more.

Take, fixed indexed annuities, for example.

They have seen average returns ranging from 3% to 7% annually, depending on the index they are tied to.

This is competitive, especially when considering the guaranteed income aspect and stability they provide compared to volatile market investments.

Many also worry that annuity payments won’t keep pace with inflation.

Given the history of annuities, this concern is completely justified.

But today, inflation-adjusted annuities, or COLA (Cost of Living Adjustment) annuities, help address this.

They can increase your payments by a set percentage each year.

For example, if you start with a $1,000 monthly payment and have a 2% COLA, your payment would increase to $1,020 the next year, then $1,040.40 the following year, and so on.

Then there’s the notion that annuities are too complex to understand.

It's a fair point – most financial products can often be overwhelming.

But, let me add, annuities have evolved.

Today, they come with clearer terms and more straightforward options.

I promise I can explain annuities in a way that makes sense, breaking down the types and benefits in a way you can easily grasp.

Remember, knowledge is power, especially when it comes to your retirement planning.

Lastly, some people don't fully understand the primary purpose of their annuity.

Again, it's understandable, given the array of financial products out there.

But here's the key point: annuities are primarily about providing a stable, continuous income stream, especially during retirement.

They're designed to give you financial peace of mind in your golden years, ensuring that you have a steady flow of income to cover your needs, no matter what the market does.

I've advised over 40,000 financial advisors and helped clients invest hundreds of millions in annuities.

I've seen firsthand how annuities can transform retirement plans.

More and more folks are moving their money into annuities for a secure, worry-free retirement.

Why People Are Flocking To GICs

In 2022, while the Nasdaq Composite was down a whopping 33.1%, and the S&P 500 dropped by 19.4%...

Money going into annuities skyrocketed.

We're talking a 23% increase, reaching an astounding $312 billion that year alone!

So why are people flocking to annuities?

It’s simple – they are dependable in an uncertain world.

For instance, some annuities offer guaranteed rates as high as 5.20% for seven years.

That’s a lot better than what you might get from CDs or Treasuries.

And when you compound these differences over the years… the results is an extra tens of thousands of dollars in your pocket.

But let’s dive deeper into more reasons why annuities are becoming the go-to for a worry-free retirement:

1. Guaranteed Income for Life:

Think of your annuity as a lifetime paycheck.

It's the only financial product out there that can promise you a set income for as long as you live.

You won't have to worry about running out of money.

2. Principal Protection:

In your annuity, your initial investment is safe from market losses.

This means you can sleep well at night knowing your capital is secure.

You only "draw down" the balance when you start taking income, and then income never goes down.

3. Tax-Deferred Growth:

Inside your annuity, you don't pay taxes on your earnings until you withdraw them.

This can mean a bigger nest egg over time.

4. Customization and Flexibility:

The beauty of annuities is that you can tailor them to your needs.

5. Balanced Portfolio:

Adding annuities to your investment mix can smooth out the ups and downs of stocks and bonds.

They provide a steady income that doesn't depend on how the market's doing.

6. Hassle-Free Investing:

Annuities are low-maintenance. You don’t have to keep an eye on them all the time.

They take the stress out of planning and managing your retirement income.

It is truly set it and forget it, while you collect paychecks from the mailbox every month.

7. Long-Term Care Benefits:

As healthcare costs rise, annuities can be a lifeline.

They can cover long-term care expenses, increase payouts if you get seriously ill, and protect your assets from being eaten up by healthcare costs.

8. Competitive Returns:

Once you've chosen to use annuities, you can often get better returns than other fixed-income products.

Most even offer a guaranteed minimum return, so you always know exactly what you're getting.

9. Peace of Mind:

Perhaps the best part – annuities offer a sense of security.

Knowing you have a reliable income to cover your basic needs brings not just financial stability but also happiness and satisfaction from making a wise financial decision.

The above reasons explain why more and more Americans are shifting their money into annuities.

It's not just a trend – it’s a movement towards a more secure retirement.

When you know you have a paycheck arriving in your mailbox every month... it's like a heavy burden has been lifted off their shoulders.

You can sleep more soundly, knowing that your financial future is more secure.

You start your mornings with a smile... enjoying my coffee a little more... knowing you've made a savvy investment.

You'll be planning trips and hobbies with excitement.

Friends and family look up to you. They come to you for advice and inspiration.

Because GICs not only secure your retirement, they show you can plan smartly, too.

Let’s Get You Set Up With Your Very Own GIC

Like I said, I want to help over 1,000,0000 American retire worry-free and never run out of money.

That’s why I wrote a book to turn that dream into your reality.

It’s called "How to Stay Rich in Retirement.”

You might have seen other retirement planning books on Amazon. You might even have read some.

But “How To Stay Rich in Retirement”

is the first and only of its kind.

I've distilled over a decade of expertise and "insider secrets" into a guide that's both deeply insightful and refreshingly simple to follow.

It walks you through each step of setting up your annuity.

It’s easy to think the whole system is just too complex and set up against you.

But this book changes that. It takes just one hour to read.

It’s simple, short, and gets straight to the point about everything you need to know.

Imagine that – just one hour to get a grip on the most important decision of the rest of your life: your retirement income.

It’s like flipping a switch to turn on a steady stream of income that you never have to worry about again.

“Embrace A Future Where You Wake Up Each Day With A Sense Of Security And Freedom."

The above is my promise.

See: you're not just getting a book. You're unlocking a new chapter in life.

Normally, a retirement guide of this caliber should cost an arm and a leg.

But today, it's available to you for just $5.60.

Because I want to reach as many everyday Americans as possible.

I've seen a lot of ways folks try to learn the ins and outs of annuities.

Let me share some thoughts on the alternatives out there:

First, there are financial advisors.

They can be helpful, but here's the catch - sometimes they have their own agendas.

Not all financial advisors like annuities because it doesn't pay them as well. It's unfortunate but true.

They might push you towards options that earn them more, like managed portfolios, and not always tell you everything about annuities.

And, as you may know, their typical 1%-2% fees can really add up over the years.

And they get rich every single year off of your investment, whether they make you money or not.

When it comes to seminars and workshops… these events might sound like a good place to learn.

But sometimes this is exactly where to find the advisors who won't tell you about annuities.

The expertise of the speakers often doesn't stack up to what I've learned in my years in finance.

Now, compare that to "How to Stay Rich in Retirement."

I'm giving you straight, unbiased advice for just $5.60. And you can get through it in about an hour.

It's a quick, affordable way to learn what you really need to know about annuities.

Think about it.

For the cost of a quick lunch, you're gaining access to strategies that can shape the rest of your life.

I'm so confident in the value this book offers that I'm giving you a full year's money-back guarantee.

If you don't find it helpful, just send me an email, and I'll refund your $5.60, no questions asked.

It's a risk-free investment in your future.

Imagine You're Looking At

A Financial Crossroad

One path leads to a future where you're always guessing about money.

The other? A bright, secure path where your golden years shine with peace and comfort.

Imagine waking up every day in retirement, not fretting over the ups and downs of the market.

Instead, you'll have a steady stream of income, just like clockwork. A reliable paycheck that keeps coming, rain or shine.

Don't wait any longer.

Click below and claim your copy of “How To Stay Rich In Retirement".

Sincerely,

Sterling Van Gogh

Annuity Facts Now and The Retirement Income Planning Association are public service companies on a mission to educate you with the truth about retirement income and annuities.

Annuity Facts Now & The Retirement Income Planning Association | 2921 W. 38th Ave #319 | Denver, CO 80211

service@annuityfactsnow.com | (720) 370-5819

Copyright Annuity Facts Now | All rights reserved

This site is not a part of the Facebook website or Facebook Inc. Additionally, this site is NOT endorsed by Facebook in any way.

FACEBOOK is a trademark of FACEBOOK, Inc.

Briggs Media, Annuity Facts Now, and The Retirement Income Planning Association are not investment firms or advisors,

and do not advocate the purchase or sale of any security or investment.

Communications offered by Annuity Facts Now and the Retirement Income Planning Association, who may offer additional services. Message and data rates may apply.

Message frequency varies. Call or text (720) 370-5819. Text STOP to cancel.

DISCLAIMER:

Please understand, we do not act as an investment advisor or advocate the purchase or sale of any security or investment. Nothing you read on this page, in this book, or in your upgrades is meant to state or imply you'll make a certain amount of money, or that this information is advice to you. Nothing can be construed as investment advice or an income claim because we don't know your financial situation and it's impossible do so in this manner. If you want advice specific to you, please consult a retirement income planning professional. Your actual results will vary according to many things, including age, savings, retirement target, legacy choices, and investment choices. The average person who buys any “how to” information gets little to no results. You should be remember investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. I’m using these references for example purposes only. Because laws change rapidly, we do not guarantee the accuracy of this information or accept any damages resulting from misuse of the strategies in whole or in part, accurate or not. All the examples you read are hypothetical. We make no representation that results demonstrated are likely or acheivable in general, or specifically to you. Our work may contain errors and you shouldn’t make any investment decision based solely on what you read from us. You should never invest with money you can't afford to lose. Your retirement income decisions are ultimately and entirely up to you. If you're not willing to accept that, please DO NOT GET THIS BOOK.